For small business owners, the balance sheet is more than just a financial document; it’s a tool for making informed decisions. It helps you gauge your business’s stability, liquidity, and overall financial position, which is crucial for planning, investment decisions, and securing financing.

At Patrick Accounting, we’ve spent twenty years turning complex financial data into something easier to understand. In this article, we’re going to explore the three main parts of your balance sheet: assets, liabilities, and equity. We’ll show you why they matter and how they can give you a clearer picture of where your business stands financially.

By the end of this, you’ll have a confident understanding of your balance sheet, helping you make better informed decisions for your business.

What is a Balance Sheet

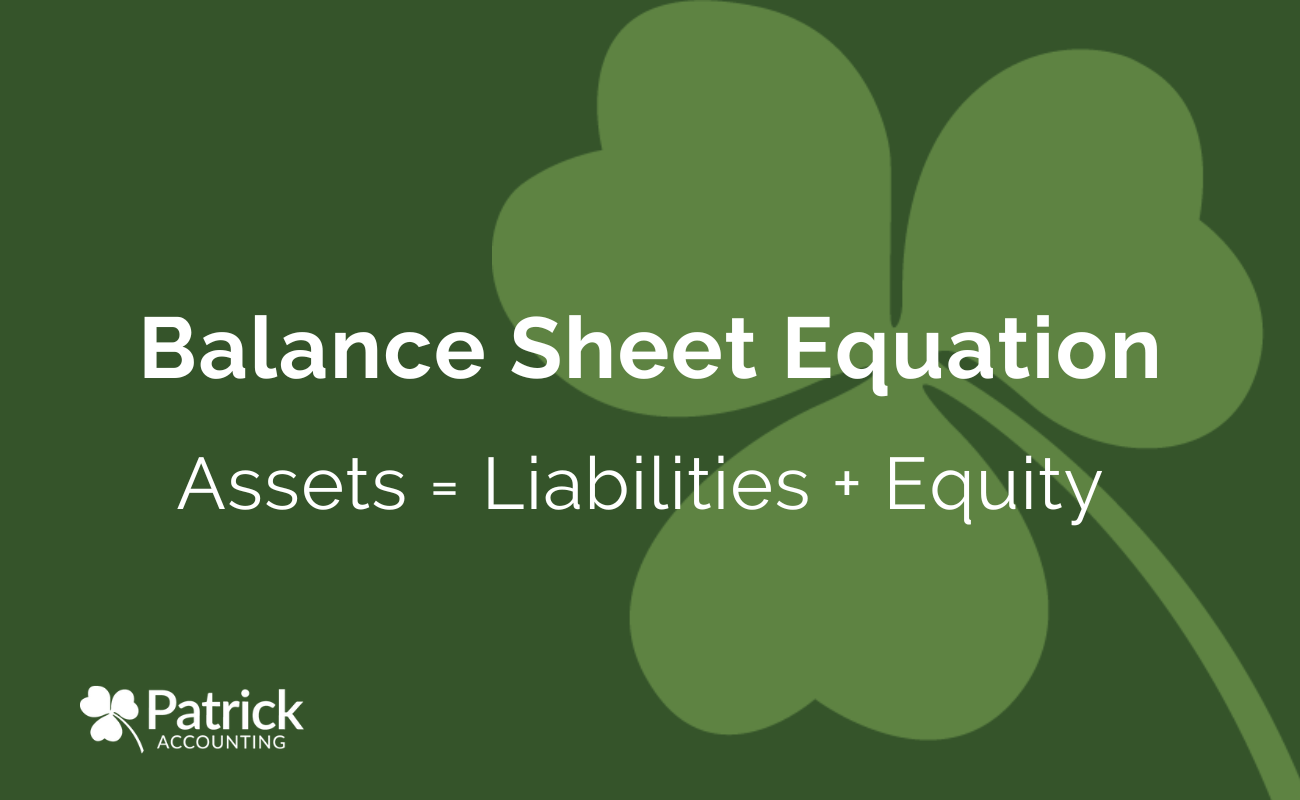

Your balance sheet is a report that shows you the financial position of your business on any given day. It reflects what your business owns (assets), what it owes (liabilities), and the value that remains with the owners (equity). It is typically generated at the end of a month, quarter, or year. The basic equation used is:

Assets = Liabilities + Equity.

Your balance sheet is a great tool to help you evaluate the overall health of your business. Potential creditors, investors, and even some customers may find it useful when they are considering whether or not to attach their hard-earned money to your company.

To truly understand your balance sheet, let’s simplify it and break down its three core components:

Assets: The Fuel for Your Small Business Engine

Understanding Your Assets

Assets are resources that your business owns or controls, expected to provide future economic benefits. In other words, these are things your business owns that have future value. If you can sell it or trade it at some point to get something else you want…it’s an asset. (Unfortunately, your winning smile and killer charm–though they may be assets socially–don’t qualify here.)

Types of Assets

Current Assets

These are assets that can be converted into cash within a year. Examples include:

- Cash (money in your bank accounts)

- Accounts Receivables (money owed to you by your customers)

- Inventory (items you intend to sell or supplies/materials that will be used in production)

Fixed Assets

Also known as non-current assets, these assets are used over time and are essential for the long-term operations of the business. These are not expected to be converted into cash within the business’s next fiscal year. Examples include:

- Property

- Buildings

- Equipment

- Long-term investments

Remember that assets are not just confined to what’s tangible – they’re also the intangible elements that contribute to your business’s value.

Liabilities: Understanding What You Owe

Liabilities represent what your business owes to others – the obligations that you are required to fulfill in the future. Simply put, anything you owe someone else is a liability. (The slacker nephew you never should have hired may also be considered a different kind of liability, but there’s just not a way to write that on your Balance Sheet!)

Think of liabilities as the opposite of assets – they’re anything that will incur an expense or cost in the future. A debt or amount owed is a liability.

Current Liabilities

Current liabilities are obligations that your business is expected to settle within the next year. Examples include:

- Accounts Payable: The amounts your business owes to suppliers or creditors for goods and services received but not yet paid for.

- Short-term Loans: Loans that your business needs to repay within the upcoming year.

- Accrued Payroll Taxes: This includes payroll taxes that have been collected from your employees but not paid to the government yet.

- Customer Deposits: Money received from customers for services or products that have not yet been delivered or completed.

Non-Current Liabilities

These are any obligations that extend beyond one year. These would typically include:

- Total Loan Amounts Due: This can be split into two parts:

- The portion of the loans that is due within the next year would fall under current liabilities.

- The remaining balance, which is due after one year, should be classified as non-current liabilities.

Equity: Your Business’s Net Worth

This is the good stuff! It represents the value that the business owners or shareholders would theoretically receive if all assets were liquidated and all debts paid off.

What Is Equity?

At its core, equity signifies the remaining interest in the company once all liabilities are subtracted from assets. It’s the net value that belongs to the owners—it’s what you, as a business owner, truly “own” in your company. Equity fluctuates as it’s influenced by the business’s operational success and financial activities. Revenue generation boosts equity, whereas expenses and owner withdrawals reduce it.

Components of Equity

- Invested Capital: The initial and subsequent investments made into the business.

- Retained Earnings: These are the profits your business has earned and retained, rather than distributed to owners or shareholders. Retained earnings demonstrate the business’s ability to generate profit and its decision to reinvest that profit for future growth.

- Net Profit: The current profit, after all expenses have been deducted from revenue, which contributes to the equity.

Equity account names can vary depending on entity type and number of owners.

It’s important to note that equity reflects the book value of your business, which may differ from its market value due to various factors like asset depreciation or appreciation.

Get to Know Your Business Better

Now that you’ve got the hang of your balance sheet, you’re on your way to really understanding what’s going on with your business’s money.

So, what’s next? Maybe you’re thinking about how to use what you own to grow your business or how to tackle debts smartly. It’s all about making those numbers work for you. And if you’re curious about how your earnings and spending play a role in all this, why not check out our related article on How to Understand Your Income Statement?

We get it – diving into these financial details can feel like a lot. At Patrick Accounting, we’re all about breaking it down and keeping it straightforward. We’re not just here to help you understand your balance sheet; we’re here to guide you through all those big financial decisions, making sure you feel confident and clued up every step of the way.

{kind=link}